Rising Incidence of Cancer

The increasing prevalence of cancer worldwide is a primary driver of the Chemotherapy Market. According to recent statistics, cancer cases are projected to rise significantly, with estimates suggesting that by 2040, the number of new cancer cases could reach 29.5 million annually. This alarming trend necessitates the development and administration of effective chemotherapy treatments, thereby propelling market growth. The Chemotherapy Market is responding to this demand by innovating and expanding treatment options, including targeted therapies and combination regimens. As healthcare systems adapt to manage this growing burden, investments in chemotherapy research and development are likely to increase, further enhancing the market landscape. The urgency to address cancer's impact on public health underscores the critical role of chemotherapy in treatment protocols, making it a focal point for pharmaceutical companies and healthcare providers alike.

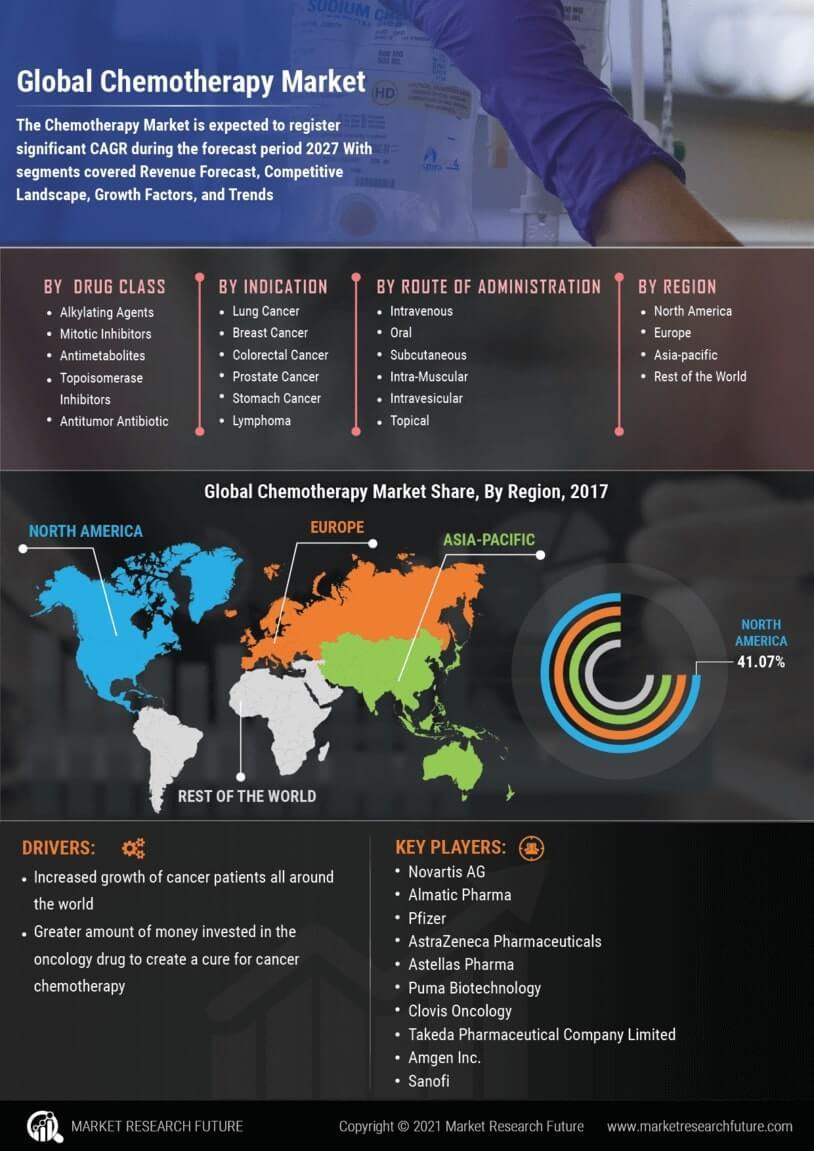

Advancements in Drug Development

Innovations in drug development are significantly influencing the Chemotherapy Market. The advent of novel therapeutic agents, including immunotherapies and targeted therapies, has transformed the treatment landscape for various cancers. Recent advancements in biotechnology and pharmacogenomics have enabled the creation of more effective and less toxic chemotherapy agents. For instance, the introduction of antibody-drug conjugates has shown promise in improving patient outcomes while minimizing side effects. The Chemotherapy Market is witnessing a surge in clinical trials aimed at evaluating these new therapies, with a notable increase in investment from pharmaceutical companies. This focus on research and development is expected to yield a pipeline of innovative treatments that could reshape the market dynamics. As these advancements continue to emerge, they are likely to enhance the efficacy of chemotherapy, thereby attracting more patients and healthcare providers to these novel solutions.

Growing Awareness and Screening Programs

The rising awareness of cancer and the importance of early detection are driving the Chemotherapy Market. Public health initiatives and educational campaigns have led to increased participation in screening programs, resulting in earlier diagnoses of various cancers. This trend is crucial, as early-stage cancers often require chemotherapy as part of the treatment regimen. The Chemotherapy Market benefits from this heightened awareness, as it translates into a larger patient population seeking treatment. Moreover, healthcare providers are increasingly recommending chemotherapy as a viable option for patients diagnosed at earlier stages, further propelling market growth. The integration of screening programs into healthcare systems is likely to continue, fostering a culture of proactive health management. As awareness grows, the demand for effective chemotherapy solutions is expected to rise, creating opportunities for pharmaceutical companies to expand their offerings in this competitive market.

Increasing Investment in Cancer Research

The Chemotherapy Market is experiencing a surge in investment directed towards cancer research and development. Governments and private organizations are recognizing the urgent need to combat cancer, leading to increased funding for research initiatives. For instance, funding for cancer research in the United States has seen a steady rise, with the National Cancer Institute's budget reaching approximately 6.56 billion USD in recent years. This influx of capital is facilitating the exploration of new chemotherapy agents and treatment modalities. The Chemotherapy Market stands to benefit from these investments, as they enable the acceleration of clinical trials and the development of innovative therapies. Furthermore, collaborations between academic institutions and pharmaceutical companies are becoming more prevalent, fostering an environment conducive to groundbreaking discoveries. As research continues to advance, the market is likely to witness the introduction of novel chemotherapy options that could significantly improve patient outcomes.

Regulatory Support and Approval Processes

Regulatory support plays a pivotal role in shaping the Chemotherapy Market. Streamlined approval processes for new chemotherapy agents are encouraging pharmaceutical companies to invest in research and development. Regulatory agencies are increasingly adopting expedited pathways for promising therapies, which can significantly reduce the time it takes for new treatments to reach the market. This trend is particularly evident in the approval of breakthrough therapies and orphan drugs, which are designed to address unmet medical needs. The Chemotherapy Market is likely to benefit from these regulatory advancements, as they facilitate quicker access to innovative treatments for patients. Additionally, the emphasis on patient-centric approaches in regulatory frameworks is fostering a more responsive environment for drug development. As regulatory bodies continue to support the introduction of new therapies, the market is expected to expand, providing patients with a broader array of chemotherapy options.